Executive Summary

The global oxalic acid market represents a mature yet dynamically evolving segment within the broader specialty chemicals industry. Characterized by its diverse applications across pharmaceuticals, electronics, metal processing, and textiles, the market is underpinned by a complex global supply chain where distribution plays a critical role in connecting concentrated production hubs with fragmented end-users. This exhaustive investment-grade analysis provides a comprehensive evaluation of the oxalic acid distribution ecosystem, synthesizing market data, competitive dynamics, regulatory pressures, and strategic forecasts to inform high-stakes investment and operational decisions.

Core Market Metrics and Growth Trajectory

The global oxalic acid market was valued at approximately USD 3.94 billion in 2024 and is projected to reach USD 5.38 billion by 2031, expanding at a steady Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period (2025–2031) (Source: S-01). Alternative analyses project a higher baseline, estimating the 2024 market at USD 15.9 billion, growing to over USD 19 billion by 2029 at a CAGR exceeding 4.0%, reflecting differences in market scope and segmentation methodologies (Source: S-02). This growth is fundamentally driven by escalating demand from key end-use industries, particularly pharmaceuticals (the largest downstream segment, accounting for ~24% of demand) and the rapidly expanding lithium-ion battery sector (Source: S-01).

Primary Market Drivers

- Expansion in High-Value End-Use Sectors: The pharmaceutical industry’s relentless growth, coupled with oxalic acid’s role as a chelating agent and precursor in drug synthesis, constitutes the single most significant demand driver. Concurrently, the global push for electrification and energy storage is fueling unprecedented demand for high-purity oxalic acid in the production of lithium battery cathode materials, representing the fastest-growing application segment (Source: S-01).

- Industrialization and Infrastructure Development in Emerging Economies: Rapid industrialization in the Asia-Pacific (APAC) region, particularly in China and India, drives demand for oxalic acid in metal cleaning, textile processing, and rare-earth element extraction. APAC dominates the market, accounting for approximately 80% of global consumption (Source: S-01, S-03).

- Technological Advancements in Sustainable Production: Growing regulatory and consumer pressure for green chemistry is catalyzing R&D into bio-based and electro-chemical production methods. Innovations such as bipolar membrane crystallization aim to reduce the environmental footprint of traditional, carbon-intensive processes like the sodium formate method, potentially reshaping cost structures and supply security in the long term (Source: S-07).

Key Market Restraints and Challenges

- Stringent and Divergent Regulatory Frameworks: The industry navigates a complex web of regulations, including EPA pesticide reregistration in the U.S., REACH compliance in the EU, and anti-dumping duties. Notably, the European Commission maintains anti-dumping duties ranging from 14.6% to 52.2% on Chinese oxalic acid and 22.8% to 43.6% on Indian oxalic acid, directly impacting trade flows and regional pricing (Source: S-05, S-06).

- Volatility in Raw Material and Energy Inputs: Oxalic acid production is energy-intensive and reliant on feedstocks like sodium hydroxide and carbon monoxide. Fluctuations in the prices of these commodities, alongside rising global energy costs, exert significant margin pressure on producers and, by extension, distributors (Source: S-02).

- Intrinsic Product Hazards and Supply Chain Complexity: Oxalic acid is a corrosive substance classified in Toxicity Category I, demanding specialized handling, storage, and transportation (Hazmat logistics). This increases operational costs for distributors and imposes stringent liability and insurance requirements, acting as a barrier to entry for less-capitalized players (Source: S-06).

Fastest-Growing Segment and Regional Hotspot

The high-purity/refined oxalic acid segment is projected to be the fastest-growing category, driven by demand from the electronics and pharmaceutical industries. This segment, valued at an estimated USD 625.5 million in 2025, is forecast to grow at a CAGR of 5.8% through 2033, reaching USD 980.2 million (Source: S-08). Geographically, while China remains the production and consumption powerhouse, Southeast Asia (e.g., Laos, Vietnam, Myanmar) is emerging as a high-growth demand hotspot, fueled by agricultural and industrial expansion and serving as a major destination for Chinese exports (Source: S-02).

High-Conviction Strategic Outlook

The oxalic acid distribution landscape is poised for a period of accelerated consolidation and strategic realignment. Megatrends including supply chain regionalization (friend-shoring), the ESG imperative, and digitalization will be key differentiators. Distributors with deep technical expertise, robust ESG credentials, and advanced digital supply chain platforms will capture disproportionate value. Furthermore, the industry must prepare for potential “black swan” disruptions, such as a sharp acceleration in bio-based production technology that could disintermediate traditional chemical routes. Over the 10-year horizon, the most successful players will be those that evolve from pure logistics providers to integrated solutions partners, offering formulation support, regulatory guidance, and closed-loop recycling services. The market outlook remains positive, albeit with clear winners and losers determined by strategic agility and operational excellence.

1. Introduction: The Oxalic Acid Market in Context

Oxalic acid (ethanedioic acid, C₂H₂O₄) is a simple yet industrially vital organic dicarboxylic acid. Its chemical properties—including strong chelating ability, reducing power, and acidity—underpin a remarkably broad spectrum of applications. Historically used in textile bleaching and metal cleaning, its utility has expanded into advanced sectors such as pharmaceutical synthesis, rare-earth processing, and lithium-ion battery manufacturing.

This report moves beyond a generic market analysis to conduct a forensic examination of the global oxalic acid distribution network. This network is the critical intermediary between a production base concentrated in Asia and a globally dispersed, fragmented end-user base. The distribution channel is not a passive pipeline but a value-adding layer responsible for logistics, technical support, regulatory compliance, and risk management. Understanding the dynamics within this layer—the competitive forces, margin structures, regulatory hurdles, and technological disruptions—is essential for stakeholders across the value chain, from producers and distributors to investors and end-users.

The analysis period, 2025–2035, captures a decade of anticipated transformation, where legacy industry structures will be tested by geopolitical shifts, sustainability mandates, and technological innovation.

2. Market Dynamics & Segmentation

2.1. Market Size, Historical Growth, and Forecast

The oxalic acid market exhibits steady, moderate growth anchored in its established industrial uses while being propelled by emerging applications. As cited, the market size in 2024 is estimated between USD 3.94 billion (QYResearch) and USD 15.9 billion (Xinsijie), with the variance attributable to differing methodologies—the former likely focusing on merchant sales of pure oxalic acid, while the latter may encompass broader downstream product values or different purity grades (Source: S-01, S-02).

The consensus CAGR for the core market through the early 2030s falls within the 4.0% to 4.6% range. This growth is not uniform across segments or regions. The refined oxalic acid segment, essential for electronics and pharmaceuticals, is forecast to grow at a premium rate of 5.8% CAGR (2025-2033), highlighting the value migration towards higher-purity, performance-critical grades (Source: S-08).

2.2. Analysis of Market Drivers

- Pharmaceutical and Electronics Industry Demand: The pharmaceutical sector’s ~24% share of downstream demand is a primary anchor. Oxalic acid is used in the synthesis of antibiotics, vitamins, and other active pharmaceutical ingredients (APIs). In electronics, it is crucial for circuit board etching and, increasingly, as a precursor in lithium cobalt oxide (LCO) and other cathode materials. The global battery market’s exponential growth directly translates into increased consumption of high-purity oxalic acid.

- Industrial Growth in APAC: The region’s dominance is self-reinforcing. China is both the world’s largest producer (with firms like Longxiang Industrial holding ~20% global market share) and consumer (Source: S-03). Infrastructure development, manufacturing expansion, and government support for downstream industries (e.g., EVs, rare-earth processing) ensure sustained demand growth within the region.

- Substitution and New Application Development: Oxalic acid is gaining ground as a “greener” alternative to harsher mineral acids in certain cleaning and leaching applications. Research into its use in carbon capture (via stable calcium oxalate formation) and as a biodegradable chelant presents potential new demand vectors in the future (Source: S-07).

2.3. Analysis of Market Restraints and Mitigation Strategies

- Regulatory Compliance Costs: The cost of complying with regulations like REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) in the EU is substantial, requiring significant investment in testing, data compilation, and regulatory affairs staff. Mitigation Strategy: Leading distributors invest in in-house regulatory teams and digital compliance platforms to streamline processes for themselves and their suppliers, turning a cost center into a value-added service.

- Trade Barriers and Geopolitical Friction: Anti-dumping duties, such as the EU’s 37.7% duty on Shandong Fengyuan and 52.2% on other Chinese firms, disrupt traditional trade patterns and increase landed costs for European consumers (Source: S-05). Mitigation Strategy: Distributors and consumers are diversifying supply sources, exploring production in duty-free regions (e.g., Southeast Asia), or engaging in strategic stockpiling. Global distributors with multi-regional hubs are best positioned to navigate these shifts.

- Raw Material and Energy Price Volatility: The sodium formate production route, a major method, is sensitive to the prices of sodium hydroxide and carbon monoxide. Energy represents a major operational cost for both production and distribution. Mitigation Strategy: Forward contracting for key feedstocks, investments in energy-efficient logistics (e.g., optimized routing, intermodal transport), and, for producers, exploring alternative, less feedstock-intensive production routes (e.g., carbohydrate oxidation) are critical risk management tools.

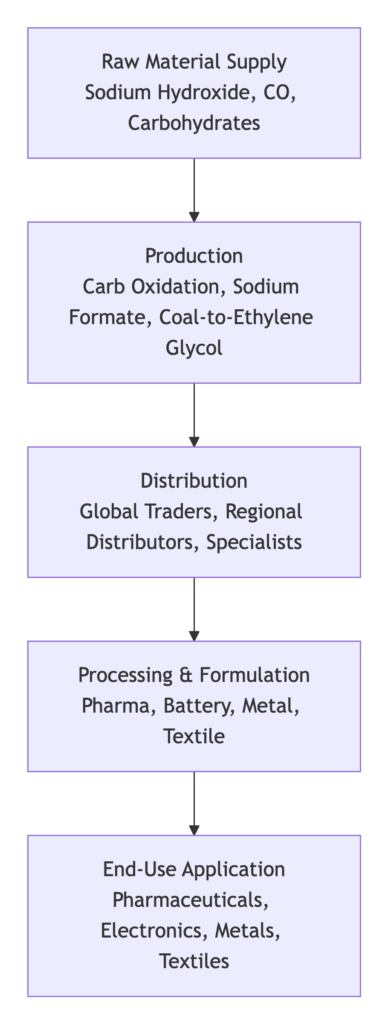

3. Deep Dive: Value Chain Analysis

The oxalic acid value chain can be deconstructed into five primary stages: Raw Material Supply, Production, Distribution, Processing/Formulation, and End-Use Application. Each stage has distinct economics, key players, and margin profiles.

1. Raw Material Supply: Upstream inputs include sodium hydroxide (caustic soda), carbon monoxide, and carbohydrates (e.g., corn starch). The supply and pricing of these commodities, particularly sodium hydroxide, have a direct and significant impact on production economics. For instance, global sodium hydroxide capacity grew at a 4-6% CAGR from 2012-2022, with Asia holding a 63.7% share, influencing regional cost advantages (Source: S-02).

2. Production: This capital-intensive stage is characterized by several competing technologies:

* Carbohydrate Oxidation: The dominant method (~60% share), using nitric acid to oxidize carbohydrates. It offers high efficiency and relatively lower cost but faces environmental scrutiny (Source: S-01).

* Sodium Formate Method: A traditional route facing pressure due to its environmental footprint and raw material volatility.

* Coal-to-Ethylene Glycol Route: Significant in China, leveraging the country’s coal resources.

* Emerging Bio-based & Electrochemical Routes: Focused on sustainability but currently at pilot or early commercial scale.

3. Distribution: This is the core focus of this report. The distribution layer includes:

* Global Chemical Distributors: Mega-players like Brenntag and Univar Solutions who offer oxalic acid as part of a vast portfolio. They compete on global network reach, logistics excellence, and one-stop-shop convenience.

* Regional/Niche Specialists: Firms that focus on specific regions (e.g., India, Southeast Asia) or end-use verticals (e.g., pharmaceuticals, electronics), competing on deep technical knowledge and customer intimacy.

* Traders and Agents: Facilitate bulk, often cross-border, transactions but typically add less technical value.

4. Processing/Formulation: Distributors or end-users often further process oxalic acid into specific formulations: solutions of precise concentration, blends with other acids, or salts like ammonium oxalate for niche applications. This stage adds significant value and requires technical capability.

5. End-Use Application: The final stage where value is realized. Margins here are highest in performance-critical applications like pharmaceutical synthesis and battery materials, where product quality and consistency are paramount.

Value Chain Insights & Pressure Points:

- Margin Compression: Intense competition among producers, especially in China, keeps upstream margins tight. Distributors face pressure from both producers seeking volume and end-users seeking cost reduction.

- Bottlenecks: Specialty logistics for hazardous materials and regulatory compliance are key bottlenecks. Distributors with certified storage facilities, Hazmat transport capabilities, and regulatory expertise control these chokepoints and capture corresponding value.

- Vertical Integration Opportunities: Some large end-users or distributors may backward integrate into formulation or even small-scale production of specialty grades to secure supply and capture margin. Conversely, large producers may forward integrate into distribution for key regions or segments to gain direct market access.

4. Hyper-Segment Analysis

4.1. By Product Type (Production Method)

- Carbohydrate Oxidation-Derived Oxalic Acid: Holds the largest share (~60%). Its cost-effectiveness ensures dominance in standard industrial applications but faces growing environmental headwinds (Source: S-01).

- Sodium Formate-Derived Oxalic Acid: A mature technology with a significant share, but its growth is constrained by environmental regulations and feedstock price volatility.

- Coal-to-Ethylene Glycol Derived Oxalic Acid: Almost exclusively in China. Its future is tied to Chinese energy policy and the evolution of its coal chemical industry.

- High-Purity/Refined Oxalic Acid: The premium, high-growth segment (>5.8% CAGR). Demand is driven by pharmaceutical GMP requirements and electronics industry specifications for ultra-low metal ion content (Source: S-08).

4.2. By Application (End-Use Industry)

- Pharmaceuticals: The largest single segment (~24% share). Demand is inelastic and quality-sensitive, supporting higher margins. Used as an API intermediate, chelating agent, and in purification processes (Source: S-01).

- Electronics & Lithium Batteries: The fastest-growing application. Used in PCB etching, semiconductor cleaning, and as a crucial precursor for lithium battery cathode materials (e.g., lithium cobalt oxide).

- Metal Processing & Rare Earths: Used for rust removal, metal cleaning, surface treatment, and as a leaching agent for rare-earth element extraction. Growth is linked to global industrial activity and the green energy transition.

- Textiles: A traditional use for bleaching and dyeing. Growth is mature and tied to the textile industry’s cyclical dynamics.

- Other Applications: Includes wood bleaching, household cleaning products, and as a reagent in fine chemical synthesis.

4.3. By Distribution Channel

- Direct Sales from Producer to Large End-User: Common for large-volume, long-term contracts in industries like metal processing or for dedicated supply to a major pharmaceutical manufacturer.

- Distribution via Global Mega-Distributors (Brenntag, Univar, etc.): The dominant channel for serving a fragmented customer base across multiple industries and regions. They provide value through logistics, inventory management, and technical support.

- Online Chemical Marketplaces (e.g., Alibaba, specialized B2B platforms): Growing in importance for smaller-volume, spot purchases, especially for standard grades. They increase price transparency but often lack value-added services.

- Specialty & Regional Distributors: Critical for accessing niche markets or regions where global players have less density. They compete on deep local knowledge, relationships, and specialized technical service.

4.4. By Region

- Asia-Pacific (APAC): The undisputed center of gravity, accounting for ~80% of global consumption and dominated by China. It is the largest producer, consumer, and exporter. Southeast Asia is a high-growth import market (Source: S-01, S-02).

- Europe: A mature market with stringent regulations. Growth is modest, driven by pharmaceuticals and specialty chemicals. The market is heavily influenced by EU trade defenses against Asian imports (Source: S-05).

- North America: A steady market with demand driven by pharmaceuticals, metal industries, and niche applications. Supply is a mix of domestic production and imports from Asia and Europe.

- Rest of World (RoW): Markets in Latin America, the Middle East, and Africa are smaller but growing, often served through regional distributors or branches of global players.

4.5. By Purity Grade

- Industrial Grade (≥98% purity): Used in metal cleaning, textile processing, and general industrial applications. The largest volume segment, characterized by high competition and lower margins.

- Technical Grade (≥99% purity): Used in more demanding applications like certain chemical syntheses and initial rare-earth processing.

- Pharmaceutical/Elexctronic Grade (≥99.6% purity): The highest specification, requiring stringent control over impurities, heavy metals, and particulates. Commands a significant price premium and is the focus of most R&D and quality investment.

5. Geopolitical & Regulatory Landscape

5.1. Regulatory Frameworks by Region

- United States: Oxalic acid is regulated as a pesticide by the Environmental Protection Agency (EPA) under the Federal Insecticide, Fungicide, and Rodenticide Act (FIFRA). It has undergone reregistration, with specific label requirements for its use as a disinfectant and sanitizer. The EPA classifies it as a Toxicity Category I substance for acute eye and skin irritation, mandating strict handling protocols (Source: S-06).

- European Union: Governance falls under the REACH regulation and the Classification, Labelling and Packaging (CLP) regulation. Any manufacturer or importer placing more than one tonne per year on the EU market must comply with extensive registration, evaluation, and safety assessment requirements. Furthermore, oxalic acid is subject to ongoing anti-dumping measures, with definitive duties imposed on imports from China and India since 2012, recently reaffirmed until at least 2029 (Source: S-05).

- China: Domestic regulations focus on environmental protection, workplace safety, and product quality standards. As the global production hub, China’s internal environmental policies (e.g., “Dual Carbon” goals) directly impact global supply availability and cost.

5.2. Geopolitical Risks and Trade Dynamics

- US-China Tensions: While oxalic acid itself has not been a primary tariff target, broader trade tensions contribute to supply chain uncertainty and promote regionalization (“friend-shoring”) efforts. Companies are assessing alternative supply sources outside China for strategic categories.

- EU Trade Defenses: The persistent anti-dumping duties against Chinese and Indian oxalic acid have permanently altered trade flows. They have protected some EU production but also raised costs for downstream EU industries. This has incentivized Chinese producers to invest in finishing capacity in Southeast Asia or other regions to circumvent duties.

- Regional Integration Agreements: Agreements like the Regional Comprehensive Economic Partnership (RCEP) in Asia can facilitate trade in chemicals among member states, potentially reshaping regional distribution networks and favoring distributors with a presence inside these trade blocs.

5.3. Impact of ESG and Sustainability Policies

- EU Green Deal and Circular Economy Action Plan: These frameworks increase pressure on the chemical industry to reduce carbon footprints, increase energy efficiency, and develop bio-based alternatives. Distributors will be scrutinized on the sustainability credentials of their supply chains.

- Corporate Sustainability Reporting Directives (CSRD): Large distributors and their customers are increasingly required to report on Scope 3 emissions (which include purchased goods). This will drive demand for oxalic acid produced via lower-carbon pathways and favor distributors who can provide verified carbon footprint data.

6. Competitive Intelligence (CI): Profiling of Key Industry Players

The competitive landscape is bifurcated between major producers who often also engage in direct sales and distribution, and pure-play distributors who aggregate supply from multiple producers.

6.1. Profile of Leading Producers/Distributors

| Company | Headquarters | Role | Key Details (Market Share, Financials, Strategy) |

|---|---|---|---|

| Longxiang Industrial (龙翔实业) | China | Producer | Global market leader with ~20% share. The undisputed volume leader, benefiting from scale, integrated production, and dominance in the APAC region. Financials are not fully transparent internationally but indicative of a multi-billion RMB revenue stream from oxalic acid and related chemicals (Source: S-03). |

| Shandong Fengyuan Chemical | China | Producer | A major Chinese producer significantly impacted by EU anti-dumping duties (37.7%). Likely pursues strategies to bypass tariffs via overseas investment or focuses on domestic and non-EU export markets (Source: S-05). |

| Oxaquim | Chile | Producer/Distributor | A significant player in the Americas, often cited in market reports. Likely holds a strong position in Latin American markets. |

| Punjab Chemicals & Pharmaceuticals | India | Producer | A key Indian manufacturer, benefiting from growth in domestic demand and serving as an alternative supply source to China for global markets, albeit also subject to EU duties. |

| Star Oxochem Pvt. Ltd. | India | Producer | An important Indian producer, competing on cost and quality in the global market. |

| Ube Industries | Japan | Producer | A diversified Japanese chemical giant producing oxalic acid, likely focusing on higher-value grades for the domestic and advanced Asian markets. |

| Brenntag AG | Germany | Global Distributor | The world’s largest chemical distributor. Offers oxalic acid as part of its vast portfolio. Competitive advantage lies in its unmatched global logistics network (~17,500 employees, 74 countries), sourcing leverage, and value-added services. 2024 Group sales exceeded €16 billion. |

| Univar Solutions Inc. | USA | Global Distributor | A leading global distributor. Key competitor to Brenntag. Strengths include a strong presence in North America and Europe and a focus on digital tools for customers. Notably, its USA arm shows active import activity for oxalic acid (Source: S-04). |

| Norkem Ltd. | UK | Global Distributor | A growing global distributor with a strong focus on specialty chemicals, including oxalic acid, serving diverse sectors from pharmaceuticals to agriculture. |

| ICC Chemical Corporation | USA | Global Distributor | A major international distributor with a strong network, particularly in the Americas and Asia. |

| Helm AG | Germany | Global Distributor | A large, privately-held chemical distributor with a significant global presence and a strong trading desk for bulk chemicals. |

| Azelis | Belgium | Global Distributor | A leading innovation service provider in specialty chemicals, focusing on formulation and technical support, potentially for higher-value oxalic acid applications. |

| IMCD Group | Netherlands | Global Distributor | A global leader in sales, marketing, and distribution of specialty chemicals and ingredients, likely active in pharmaceutical and high-purity oxalic acid segments. |

| Omya AG | Switzerland | Specialty Distributor/Producer | While primarily a calcium carbonate producer, its distribution network may handle related chemicals like oxalic acid in certain regions. |

| Ashland Global Holdings | USA | Specialty Distributor/Producer | A global specialty materials company whose distribution arm may supply oxalic acid into focused end-markets like pharmaceuticals or personal care. |

| Hawkins, Inc. | USA | Regional Distributor | A major US distributor of industrial chemicals, water treatment, and specialty ingredients, with a significant role in distributing oxalic acid to industrial end-users. |

| JKM Chemtrade | India | Regional Distributor | An Indian business portal listing, representative of numerous regional distributors that form the backbone of local supply networks in emerging markets (Source: S-09). |

| T.N.C. Industrial (Tianjin) Co., Ltd. | China | Producer/Exporter | A representative example of the many Chinese chemical producers/exporters that sell directly or through traders on global B2B platforms. |

| Spectrum Chemical Mfg. Corp. | USA | Specialty Distributor | A leading supplier of fine chemicals and laboratory products, crucial for distributing pharmaceutical and reagent-grade oxalic acid to research and pharmaceutical customers. |

| VWR International (Part of Avantor) | USA | Specialty Distributor | A global distributor of laboratory supplies and chemicals, serving the research, pharmaceutical, and biotech sectors with high-purity grades. |

6.2. Recent M&A, Joint Ventures, and Strategic Moves

- Consolidation among Distributors: The distribution sector has seen sustained consolidation (e.g., Univar’s acquisition of ChemSol in 2023) to gain scale, geographic reach, and specialty capabilities (Source: S-11).

- Vertical Integration by Producers: Chinese producers may establish sales offices or joint ventures with distributors in key export markets (e.g., Southeast Asia, Africa) to gain more control over the value chain.

- Sustainability-Linked Alliances: Distributors are forming partnerships with producers investing in green chemistry to secure sustainable product lines and meet customer ESG demands.

7. Strategic Industry Frameworks

7.1. Porter’s Five Forces Analysis

- Threat of New Entrants (Low to Moderate): Barriers are significant. They include: high capital requirements for production (but lower for pure distribution); stringent regulatory and safety compliance; the need for established logistics and storage networks for hazardous materials; and the entrenched relationships of incumbents with both suppliers and customers. New entrants are most likely in niche distribution or online B2B platforms.

- Bargaining Power of Suppliers (Moderate to High): For distributors, suppliers are the producers. Power is concentrated among a few large producers in China (e.g., Longxiang). However, distributors like Brenntag have countervailing power due to their massive purchasing volume and ability to switch suppliers globally. For small distributors, supplier power is high.

- Bargaining Power of Buyers (High): Buyers are fragmented but have options. The standardized nature of industrial-grade oxalic acid makes it a commodity where price is a key decision factor. However, for high-purity grades and in regulated industries (pharma), buyers prioritize quality, reliability, and technical support, slightly reducing pure price power.

- Threat of Substitute Products (Low to Moderate): In specific applications, substitutes exist (e.g., citric acid for cleaning, other organic acids in leaching). However, oxalic acid’s unique combination of properties, effectiveness, and cost in many core applications (metal cleaning, rare-earth extraction, certain pharmaceutical syntheses) ensures its position. The threat is higher in environmentally sensitive areas where “greener” alternatives are being sought.

- Rivalry Among Existing Competitors (High): Competition is intense at both production and distribution levels. In production, Chinese firms compete fiercely on cost. In distribution, global players compete on geographic coverage, service breadth, and digital capabilities, while regional players compete on deep local knowledge and agility. Price competition is acute for standard grades.

7.2. PESTLE Analysis

- Political: Trade policies (anti-dumping duties, tariffs) are the most direct political factor. Government incentives for battery manufacturing or pharmaceuticals indirectly drive demand. Political stability in key producing (China) and consuming regions affects supply chain reliability.

- Economic: Global GDP growth drives industrial demand. Raw material (oil, coal, agriculture) and energy price inflation directly impact production costs and margins. Exchange rate fluctuations affect the competitiveness of exporters.

- Social: Increasing awareness of workplace safety and environmental protection raises standards for handling and production. The social push for sustainability influences procurement decisions.

- Technological: Advancements in bio-production (fermentation) and electrochemical synthesis could disrupt traditional production economics. Digitalization (IoT, blockchain) is transforming distribution through track-and-trace, inventory optimization, and predictive logistics.

- Legal: A dense layer of regulations governs the entire lifecycle: REACH/CLP in Europe, FIFRA in the US, GHS labeling worldwide, and transportation codes for hazardous materials (ADR, IMDG, IATA). Compliance is non-negotiable and costly.

- Environmental: The carbon footprint of production is under scrutiny. Wastewater treatment from production plants is a key environmental issue. The industry faces pressure to transition to circular economy models, including recycling of oxalate-containing waste streams.

8. Future Outlook & Disruption (2025-2035)

8.1. Megatrends Shaping the Next Decade

- Supply Chain Regionalization and Resilience: In response to geopolitical tensions and pandemic-era disruptions, end-users will seek to diversify supply sources away from over-reliance on any single region. This will benefit distributors with truly global, multi-sourcing networks and could spur new production investment in regions like Eastern Europe, North America, or India.

- The ESG Imperative: ESG performance will transition from a “nice-to-have” to a core commercial competency. Distributors will need to provide verified data on the carbon footprint, water usage, and sourcing ethics of their oxalic acid supply. Partners offering bio-based or circular-economy-derived oxalic acid will gain a competitive edge.

- Digital Transformation and Value-Added Services: The winning distributors will be those that leverage AI and data analytics for demand forecasting, inventory management, and proactive customer service. Beyond logistics, they will offer digital tools for regulatory compliance, formulation support, and environmental impact reporting.

8.2. Disruptive Technologies (Christensen’s Model)

- Potential Low-End Disruption: Microbial fermentation for oxalic acid production, currently a high-cost, niche technology, could follow a classic disruptive innovation path. It may start in small-scale, high-value applications (e.g., specialty pharmaceuticals) where its “green” credential commands a premium. With iterative improvements in yield and scale, it could eventually become cost-competitive with chemical synthesis for bulk applications, displacing incumbent producers reliant on fossil feedstocks (Source: S-07).

- E-commerce Platform Disruption: Online chemical marketplaces could disrupt traditional distributor relationships for standard-grade, transaction-based sales. However, for complex, service-intensive needs, the full-service distributor model will remain robust.

8.3. Risk-Adjusted Forecasts and “Black Swan” Events

- Base Case Forecast (70% Probability): Market grows at a ~4.5% CAGR to 2035, driven by steady demand from pharmaceuticals and batteries. Distribution remains consolidated among global players, with regional specialists thriving in niches.

- Upside Scenario (20% Probability): A breakthrough in cost-effective bio-production or a major policy push for oxalic acid in carbon capture creates a new, massive demand vector, accelerating growth to a 7%+ CAGR. Early investors in the technology reap outsized rewards.

- Downside Scenario (10% Probability): A severe global recession suppresses industrial demand. Simultaneously, a major environmental accident in the production sector triggers draconian new regulations, squeezing margins and forcing consolidation. A geopolitical conflict in Asia severely disrupts supply chains.

Conclusion: The oxalic acid distribution market is stable but not static. Success in the coming decade will require distributors to be more than just conduits for chemicals. They must become orchestrators of resilient, sustainable, and digitally-enabled supply chains. For investors, the opportunities lie in backing distributors with strong technical service models, robust ESG strategies, and the scale to navigate an increasingly complex geopolitical and regulatory world. The companies that can successfully integrate these capabilities will define the next era of the oxalic acid industry.

9. References & Sources

- S-01: QYResearch. (2025). 2025年全球草酸市场规模调查及十五五前景预测报告 (2025 Global Oxalic Acid Market Size Survey and 15th Five-Year Plan Prospect Forecast Report). QYResearch Co., Ltd. https://www.gelonghui.com/p/1993684.

- S-02: Xinsijie (新思界网). (2025-07-30). 老挝农业生产规模不断壮大 草酸市场需求增长迅速 (Laos Agricultural Production Scale Continues to Expand, Oxalic Acid Market Demand Grows Rapidly). NetEase Hao (163.com). https://www.163.com/dy/article/K5INJI9J0514E30D.html.

- S-03: Sohu. (2024-11-30). 草酸市场调研报告-主要企业、市场规模、份额及发展趋势 (Oxalic Acid Market Research Report – Major Enterprises, Market Size, Share, and Development Trends). Sohu.com. [Search Result Reference].

- S-04: Import Data. (2025-07-31). UNIVAR SOLUTIONS USA INC. import record for Oxalic Acid. [Search Result Reference].

- S-05: China Trade Remedy Information Network (中国贸易救济信息网). (2024-09-10). 欧盟对涉华草酸作出第二次反倾销日落复审终裁 (EU Makes Final Determination in Second Sunset Review of Anti-Dumping Duties on Chinese Oxalic Acid). Ministry of Commerce, China. https://cacs.mofcom.gov.cn:443/cacscms/article/ckys?articleId=181750.

- S-06: United States Environmental Protection Agency (EPA). (1992, December). Reregistration Eligibility Document (RED) Facts: Oxalic Acid (EPA-738-F-92-014). Office of Prevention, Pesticides and Toxic Substances.

- S-07: Ayere, J.E., et al. (2024, June 15). A comprehensive review of recent advances in the applications and biosynthesis of oxalic acid from bio-derived substrates. PubMed (NIH). https://pubmed.ncbi.nlm.nih.gov/ [Search Result Reference].

- S-08: ReportsInsights. (2025-11-11). 精制草酸市场2025-2033:可持续增长与核心指标研究 (Refined Oxalic Acid Market 2025-2033: Sustainable Growth and Core Indicator Research). ReportsInsights Consulting. [Search Result Reference].

- S-09: Indian Business Portal. Oxalic Acid At Jkm Chemtrade. [Search Result Reference].

- S-10: Brenntag Corporate Website. Company Profile and Distribution Network. [Search Result Reference].

- S-11: Paint.org. (2023-02-17). Univar Solutions Acquires ChemSol. https://www.paint.org/ [Search Result Reference].

Leave a Reply