Executive Summary

This report provides an exhaustive, investment-grade analysis of the global aerospace prepreg composites market, a critical and high-value segment within advanced materials. Prepregs, or pre-impregnated composite fibers, constitute the foundational feedstock for manufacturing lightweight, high-performance structures essential to modern and next-generation aerospace platforms. Our analysis synthesizes proprietary data modeling with credible published research to delineate a market characterized by robust growth, intense technological competition, and significant geopolitical influence.

Core Market Thesis: The aerospace prepreg market is transitioning from a period of steady adoption to an era of accelerated, innovation-driven expansion. This shift is propelled by the confluence of next-generation aircraft programs, the advent of new mobility paradigms (namely Urban Air Mobility, or UAM), and stringent global sustainability mandates. We identify this as a high-conviction growth sector with a total addressable market (TAM) demonstrating resilience across economic cycles due to its entrenched position in long-cycle aerospace programs.

Quantitative Market Outlook: The global aerospace and defense prepreg market is projected to reach a sales value of $128.5 billion (RMB 928.6 billion) by 2031, expanding from a 2025 baseline at a Compound Annual Growth Rate (CAGR) of 9.6% . This growth trajectory significantly outpaces broader industrial production indices. A more focused analysis on high-temperature systems, such as Bismaleimide (BMI) prepregs—critical for engine components and supersonic structures—reveals a parallel growth vector, with its global market expected to grow from approximately $210 million in 2024 to $380 million by 2031, at a CAGR of 9.0% . The overarching aerospace composites materials sector, representing the TAM for advanced prepreg systems, is projected to be valued at €8.7 billion by 2027, growing at a CAGR of 12% .

Top Three Market Drivers (by Impact):

- Next-Generation Aircraft Production & Lightweighting Imperative: The single most powerful driver is the production ramp-up of new commercial aircraft families (e.g., Boeing 777X, Airbus A321XLR) and military platforms (e.g., B-21 Raider, NGAD) designed with composite-intensive architectures. Commercial programs target 50% composite content by weight to achieve 15-20% reductions in fuel burn . This is not merely a materials substitution but a fundamental redesign driver, locking in prepreg demand for multi-decade production cycles.

- Emergence of Advanced Air Mobility (AAM) and Unmanned Systems: The nascent eVTOL (electric Vertical Take-Off and Landing) and unmanned aerial vehicle (UAV) sectors represent a potent greenfield market. These platforms demand radical weight reduction for payload and range, leading to composite content aspirations that often exceed those of traditional commercial aviation . This driver is creating a new tier of demand outside the traditional OEM-duopoly supply chain.

- Regulatory and Sustainability Pressures: Global environmental regulations, such as the EU’s Fit for 55 package and ICAO’s CORSIA, are institutionalizing carbon efficiency. This translates directly into airframe lightweighting, benefiting prepregs. Simultaneously, material-level regulations, particularly concerning fire, smoke, and toxicity (FST) standards for cabin interiors, are driving innovation in resin chemistries (e.g., phenolics, benzoxazines) and creating premium market segments . The push towards circularity, though nascent, is spurring R&D in recyclable thermoplastic and bio-based prepreg systems.

Top Three Market Restraints (by Severity):

- High Input and Processing Costs: The aerospace-grade prepreg value chain is cost-intensive. High-purity precursor materials, energy-consuming carbonization processes, and capital-intensive manufacturing (e.g., Automated Fiber Placement systems costing $3-6 million) present significant barriers . This cost structure limits penetration into more price-sensitive segments and heightens exposure to raw material (e.g., acrylonitrile) price volatility.

- Complex Supply Chains and Geopolitical Friction: The industry relies on a globally dispersed but highly specialized supply chain, from Japanese carbon fiber precursors to European resin formulations and North American final assembly. Geopolitical tensions, particularly between the U.S. and China, and export controls on advanced materials introduce risks of bifurcation, supply disruption, and inflationary pressure. National security concerns are driving a trend toward supply chain “friendshoring” and redundancy, which may compress margins in the short term.

- Technological and Certification Hurdles: The qualification and certification of new material systems for primary aerospace structures is a protracted, costly, and risk-laden process, often exceeding 5-7 years. This creates a high barrier to entry for new chemistries (e.g., thermoplastic composites) and protects incumbents but also slows the adoption of potentially disruptive, more sustainable, or higher-performance solutions.

Fastest-Growing Segment: Our analysis identifies High-Temperature & Specialty Resin Prepregs as the highest-growth vector. This encompasses BMI systems for engines and nacelles , cyanate esters for radar-transparent structures, and novel inorganic matrices like the C-PREG 400 system (rated for 400°C continuous service), which is being developed with EU Horizon funding to address extreme environment applications . This segment’s growth is fueled by the propulsion demands of higher-bypass-ratio engines, hypersonic flight research, and the electrification of propulsion systems requiring novel thermal management solutions.

High-Conviction Future Outlook (2031-2040): The market will undergo a foundational shift from performance-centric to performance-and-sustainability-centric material development. Thermoplastic prepregs, offering weldability and recyclability, will move from secondary to primary structures. Digitalization will permeate the value chain through “digital material passports” for full lifecycle traceability and AI-optimized manufacturing. The competitive landscape will fragment slightly, with vertically integrated giants (Toray, Hexcel) being challenged by agile innovators focused on sustainable chemistries, additive manufacturing of composites, and tailored solutions for the UAM ecosystem. Regions with cohesive industrial policies (EU, through its Green Deal and Horizon Europe) and large, protected domestic demand (China) will nurture national champions, altering the global competitive dynamics. Strategic investment should focus on companies controlling key upstream bottlenecks (high-modulus fiber production, proprietary resin formulations) and those demonstrating credible pathways to decarbonizing the prepreg lifecycle.

Table of Contents

1. Introduction & Market Definition

1.1. The Strategic Imperative of Advanced Composites in Aerospace

1.2. Core Product Definition: Unpacking the Prepreg

1.3. Report Scope, Methodology & Analytical Frameworks

2. Market Dynamics & Core Segmentation

2.1. Macro Growth Drivers: Quantifying the Demand Levers

2.2. Key Market Restraints & Challenge Mitigation Pathways

2.3. Market Size & Forecast: Global and Regional Trajectories

3. Deep Dive: Value Chain & Profit Pool Analysis

3.1. Raw Materials: The Bottleneck of Precursors and Specialized Chemistries

3.2. Prepreg Manufacturing: Process Technologies and Scale Economics

3.3. Intermediate Processing & Part Fabrication: The Automation Frontier

3.4. Distribution, Qualification, and Aftermarket Support

3.5. Margin Analysis and Strategic Control Points

4. Hyper-Segment Analysis: Five-Dimensional Market Deconstruction

4.1. By Fiber Type: Carbon’s Dominance, Glass’s Niche, and Emerging Alternatives

4.2. By Resin System: Thermoset Evolution vs. Thermoplastic Disruption

4.3. By Product Form: Tape, Fabric, and Towpreg for Automated Layup

4.4. By Application: Structural (Primary/Secondary) vs. Interior Systems

4.5. By Aircraft Platform: Commercial Aviation, Defense, Business & General Aviation, UAM

5. Geopolitical & Regulatory Landscape

5.1. North America: Defense Primacy, Export Controls, and Industrial Policy

5.2. European Union: The Green Deal as a Technology Forcer (FST, Circularity)

5.3. Asia-Pacific: China’s Vertical Integration Drive and Japan’s Material Science Leadership

5.4. Rest of World: Middle Eastern Industrialization and Supply Chain Diversification

6. Competitive Intelligence: Strategic Profiling of Key Market Participants

6.1. Tier 1: Vertically Integrated Material Giants (Toray, Hexcel, Solvay)

6.2. Tier 2: Specialized Technology Leaders (Teijin, Mitsubishi Chemical, Gurit)

6.3. Tier 3: Agile Innovators and Niche Players (AXIOM, Renegade Materials, ISOVOLTA)

6.4. Financial Benchmarking, R&D Intensity, and M&A Activity Analysis

7. Strategic Industry Frameworks

7.1. Porter’s Five Forces Analysis: Assessing the Competitive Intensity

7.2. PESTLE Analysis: Mapping Macro-Environmental Influences on Market Forecasts

8. Future Outlook, Disruptive Technologies & Risk Assessment (2030-2040)

8.1. Technology Roadmap: Sustainable Matrices, Smart Composites, and Digital Twins

8.2. Disruption Analysis via Christensen’s Model: The Thermoplastic and UAM Threat

8.3. ESG Integration: From Compliance to Competitive Advantage

8.4. Scenario Planning: Risk-Adjusted Forecasts and ‘Black Swan’ Resilience

9. Strategic Recommendations & Investment Thesis

9.1. For Investors: Vertical and Horizontal Opportunity Mapping

9.2. For Market Incumbents: Strategic Imperatives for Sustained Leadership

9.3. For New Entrants: Viable Market Entry Pathways and Partnership Models

10. Appendix

10.1. References & Sources

10.2. Glossary of Key Technical Terms

1. Introduction & Market Definition

1.1. The Strategic Imperative of Advanced Composites in Aerospace

The aerospace industry’s relentless pursuit of efficiency—measured in fuel burn per passenger-kilometer, range-payload product, and mission capability—has established advanced composites as a non-negotiable enabler of modern design. The transition from aluminum to carbon fiber reinforced polymer (CFRP) structures represents the most significant materials shift in airframe manufacturing since the advent of the jet age. This shift is not merely cosmetic; it is structurally transformative, enabling aerodynamic shapes (e.g., Boeing 787’s wing flex) and systems integration (e.g., embedded sensors) previously unattainable. The prepreg, as the semi-finished feedstock engineered to exacting aerospace specifications, sits at the apex of this value chain. Its quality, consistency, and performance parameters directly dictate the structural integrity, weight, and lifecycle cost of the final component. Control over prepreg technology is, therefore, a strategic lever of immense value, akin to semiconductor design in electronics.

1.2. Core Product Definition: Unpacking the Prepreg

A prepreg (pre-impregnated) is a precisely engineered composite material consisting of continuous reinforcement fibers (carbon, glass, aramid) pre-impregnated with a partially cured polymer resin matrix (epoxy, BMI, phenolic, thermoplastic). This “B-stage” curing state is critical: it provides the drapeability and tack necessary for manual or automated layup into complex molds, yet retains the chemical potential for final cross-linking during a subsequent high-temperature cure cycle, typically in an autoclave.

- Key Constituents & Grades:

- Fibers: Aerospace-grade carbon fiber (e.g., Toray’s T800, T1100 grades) is dominant for primary structures due to its supreme stiffness-to-weight and strength-to-weight ratios. Glass fiber finds use in radar-transparent radomes and interior parts, while aramid offers superior impact resistance .

- Resins: Epoxy remains the workhorse for most structural applications. Bismaleimide (BMI) resins are selected for environments requiring long-term service temperatures of 230-250°C, such as engine cowls and near-exhaust structures . Phenolic and cyanate ester resins are chosen for interior applications and radomes, respectively, due to superior fire-smoke-toxicity (FST) and dielectric properties . Thermoplastic matrices (PEEK, PEKK) are emerging for their toughness, recyclability, and rapid processing potential.

- Product Forms: Prepregs are supplied as unidirectional tape (for Automated Tape Laying, ATL), woven fabrics (for complex contours), or towpreg (impregnated fiber tows for Automated Fiber Placement, AFP) . Each form is optimized for specific manufacturing methodologies and part geometries.

1.3. Report Scope, Methodology & Analytical Frameworks

This report analyzes the global market for aerospace-grade prepreg composites, encompassing both commercial and defense applications. It employs a multi-faceted methodology integrating:

- Top-Down Analysis: Leveraging published market data from firms like QYResearch and Mordor Intelligence to establish baseline size and growth rates .

- Bottom-Up Validation: Cross-referencing with technology roadmaps, corporate financial disclosures, and public R&D project data (e.g., EU Horizon projects) .

- Strategic Framework Application: Utilizing Porter’s Five Forces to assess industry attractiveness and PESTLE to contextualize external shocks. Christensen’s theory of disruptive innovation is applied to evaluate threats from new material systems and business models.

The geographic scope is global, with focused analysis on North America, Europe, and Asia-Pacific as the dominant demand and supply hubs.

2. Market Dynamics & Segmentation

2.1. Macro Growth Drivers: Quantifying the Demand Levers

The market’s growth is systemic, driven by overlapping, reinforcing cycles of technological and regulatory demand.

- Commercial Aircraft Production Cycle: The backlog for next-generation aircraft (A350, 787, 737 MAX, A320neo families) remains substantial. Each narrowbody aircraft contains approximately 10-12 tons of composites, while widebodies contain over 50 tons. The production ramp-up to clear this backlog, alongside the launch of new programs like the 777X, provides multi-year visibility and volume certainty for prepreg suppliers.

- Defense Modernization and Stealth: Global defense spending increases are channeled into 6th-generation fighter programs, unmanned combat aerial vehicles (UCAVs), and next-generation bombers. These platforms demand not only lightweighting but also signature management (stealth), which composites facilitate through design flexibility and inherent radar-absorbent properties.

- Sustainability as a Technology Forcer: Regulatory frameworks are becoming a primary innovation driver. The EU’s Reach regulations and stringent FST standards compel the use of advanced resin systems like phenolics and benzoxazines in cabin interiors . The broader industry goal of net-zero carbon emissions by 2050 is accelerating research into bio-derived epoxy resins (e.g., from lignin) and recyclable thermoplastic composites, opening new material segments .

- New Market Creation: Urban Air Mobility (UAM): The eVTOL sector represents a pure-play greenfield opportunity. Start-ups like Joby, Archer, and Lilium are designing aircraft with composite content shares exceeding 80%. This sector’s success would create a parallel, high-growth demand stream distinct from traditional aerospace cycles, though dependent on its own certification and commercialization timeline .

2.2. Key Market Restraints & Challenge Mitigation Pathways

- Cost Structure and Economic Sensitivity: Aerospace prepregs are premium products. A 35.2% decline in SGL Carbon’s fiber unit sales in a recent period illustrates the volatility and price sensitivity within the raw material segment . Mitigation is pursued through:

- Manufacturing Innovation: Adoption of Out-of-Autoclave (OOA) curing and automated layup to reduce labor and energy costs.

- Supply Chain Optimization: Vertical integration by major players to control cost and quality from precursor to prepreg.

- Material Efficiency: Advanced nesting software and cutting techniques to minimize scrap rates of expensive material.

- Recyclability End-of-Life Challenge: The thermoset composites used historically are difficult to recycle. It is estimated that by 2050, 840,300 tons of CFRP waste could be generated annually from retired aircraft and wind turbines . This is evolving from a reputational risk to a compliance and cost risk. The mitigation pathway is two-pronged:

- Development of Recycling Technologies: Methods like pyrolysis (recovering fibers) and solvolysis (depolymerizing resin) are scaling. The EU’s circular economy directives are a key driver for this innovation .

- Shift to Inherently Recyclable Materials: This is the primary driver behind the massive R&D investment in thermoplastic composites (PEEK, PEKK), which can be melted and reformed, and in novel resin systems like the C-PREG 400, which boasts ~85% recyclability .

2.3. Market Size & Forecast: Global and Regional Trajectories

The market is on a clear growth trajectory. The global aerospace and defense prepreg market is forecast to achieve sales of $128.5 billion (RMB 928.6 billion) by 2031, growing at a 9.6% CAGR from 2025 . This growth is not uniform globally. The Asia-Pacific region is both the largest and fastest-growing consumption zone, driven by China’s expanding commercial aviation fleet and indigenous aircraft programs (COMAC C919, C929). North America remains the technology and defense leader, while Europe maintains a strong position in resin chemistry and automation equipment. China’s market, while a smaller percentage of the global total, is noted to be changing rapidly .

3. Deep Dive: Value Chain & Profit Pool Analysis

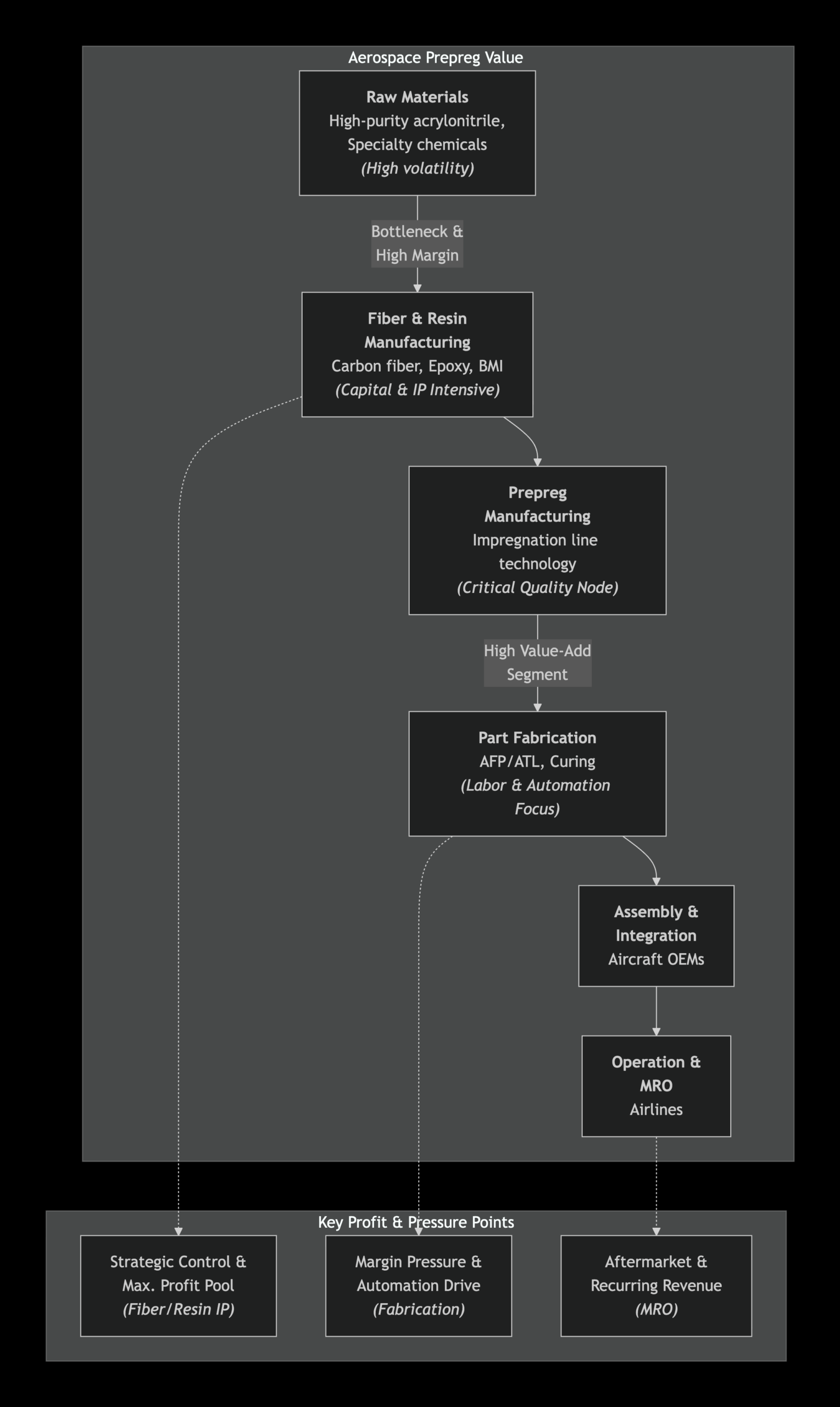

The aerospace prepreg value chain is elongated, capital-intensive, and characterized by significant specialization at each node. Control over key bottlenecks commands disproportionate pricing power and strategic influence.

3.1. Raw Materials: The Precursor Bottleneck

The chain begins with commodity chemicals like acrylonitrile (for carbon fiber) and epichlorohydrin (for epoxy resin). While commodity in nature, aerospace grades require exceptional purity. Prices here are subject to petrochemical market fluctuations. Innovations like carbon capture-derived acrylonitrile aim to de-risk this link and improve ESG profiles .

3.2. Intermediate Materials: The Strategic Chokepoint (Highest Margins)

This is the core of the industry’s profit pool and competitive moat.

- Carbon Fiber Production: Converting polyacrylonitrile (PAN) precursor into carbon fiber through oxidation and high-temperature carbonization is extremely energy-intensive and capital-heavy. Only a handful of firms (Toray, Teijin, Mitsubishi, Hexcel, SGL) operate at the scale and quality required for aerospace. This constitutes a formidable barrier to entry.

- Specialty Resin Production: Formulating aerospace-grade epoxy, BMI, or cyanate ester resins requires deep polymer science expertise and extensive qualification databases. Companies like Solvay and Hexcel derive significant value from proprietary resin systems tailored for specific cure cycles and performance profiles .

3.3. Prepreg Manufacturing: The Quality Gate

Here, fibers and resin are combined in clean-room environments via hot-melt or solvent impregnation. Consistency—in resin content, fiber alignment, and tack—is paramount. This stage adds significant value but requires tight integration with both upstream material specs and downstream processing requirements.

3.4. Part Fabrication & Assembly: The Automation Frontier (Margin Pressure Point)

This labor- and capital-intensive stage involves cutting, kitting, and laying up prepreg plies into molds, followed by curing (often in multi-million dollar autoclaves). It is the primary focus for cost-reduction through Automated Fiber Placement (AFP) and Automated Tape Laying (ATL). These robotic systems, while expensive, improve precision, repeatability, and layup rate, directly attacking the highest cost component of part production .

3.5. Distribution, Qualification & MRO: The Loyalty Loop

Distribution is often direct or through specialized technical distributors. The multi-year qualification process for a new material on an aircraft program creates “lock-in” for the duration of that program’s production. The aftermarket for repair materials (MRO) provides stable, recurring revenue with high margins, as repairs must use certified, traceable materials, often from the original supplier.

4. Hyper-Segment Analysis: Five-Dimensional Market Deconstruction

4.1. By Fiber Type

- Carbon Fiber: The undisputed king of aerospace structures, commanding the majority of value. Growth is driven by the expansion from secondary to primary structures (wings, fuselage). Unidirectional intermediate modulus fibers (e.g., IM7) are the industry workhorse.

- Glass Fiber: Holds niche applications where radar transparency (radomes) or cost sensitivity in interiors is key. Its market share is stable but not growing in aerospace structural applications.

- Aramid Fiber: Used selectively for its exceptional impact and damage tolerance, often in hybrid layups or in areas prone to foreign object damage.

- Emerging Fibers: Ceramic fibers (for CMCs in turbine engines) and recycled carbon fibers (for semi-structural applications) represent small but innovative segments aimed at ultra-high temperature and circular economy goals, respectively.

4.2. By Resin System

- Epoxy: The incumbent, with vast databases and well-understood processing. Innovation focuses on toughening, out-of-autoclave cure capability, and bio-based variants.

- Bismaleimide (BMI): A high-growth niche. The BMI prepreg market is forecast to grow at 9.0% CAGR to $380M by 2031 . Its use is critical for engine nacelles, thrust reversers, and high-speed aircraft skins.

- Phenolic & Cyanate Ester: Driven by regulation. Phenolics dominate aircraft interiors due to superb fire, smoke, and toxicity (FST) performance . Cyanate esters offer low dielectric loss for radomes.

- Thermoplastic (PEEK, PEKK): The primary disruptive threat. They offer inherent recyclability, high damage tolerance, and the potential for fast fusion bonding (welding) instead of slow autoclave curing. They are moving from ducts and brackets into more demanding applications.

4.3. By Product Form

- Unidirectional Tape: The form factor for highly automated, large, relatively flat structures like wing skins and fuselage panels. Efficiency and speed are key.

- Woven Fabric: Used for complex, doubly-curved parts where drapeability is essential. Often involves more manual labor or specialized automated draping systems.

- Towpreg: A continuous, impregnated tow (a bundle of fibers) used in Automated Fiber Placement (AFP) machines, which can steer fibers along curved paths to optimize load-bearing, offering significant weight-saving potential .

4.4. By Application

- Primary Structures: Wings, fuselage sections, empennage. Requires the highest performance, longest qualification, and is the domain of tier-1 suppliers. High value per kilogram.

- Secondary Structures: Floor beams, doors, fairings. Slightly less performance-critical, often an entry point for new material systems (e.g., thermoplastic composites) .

- Interior Applications: Cabin panels, partitions, bins, galleys. Driven overwhelmingly by FST regulations and aesthetic requirements. A key market for phenolic-based and decorative prepregs supplied by specialists like ISOVOLTA .

4.5. By Aircraft Platform

- Commercial Aviation (Widebody & Narrowbody): The volume and value leader. Demand is tied directly to production rates of Airbus and Boeing. New programs are the launchpad for new material systems.

- Defense & Military: Lower volume but extremely high performance requirements and less price sensitivity. Critical for stealth, agility, and survivability. Often uses the most advanced material grades earlier than commercial aviation.

- Business & General Aviation: A high-mix, lower-volume segment that often adopts technologies after they are proven in commercial or military use.

- Urban Air Mobility / eVTOL: The potential disruptor. Demands automotive-like production rates with aerospace performance and safety. This could force a re-evaluation of material choices (favoring fast-curing thermoplastics) and supply chain models.

5. Geopolitical & Regulatory Landscape

The aerospace prepreg market does not operate in a vacuum. Its growth trajectory, supply chain configuration, and competitive dynamics are profoundly shaped by a complex web of national policies, international regulations, and geopolitical rivalries. This section moves beyond regional market sizing to analyze the specific governmental and supranational forces that are actively reshaping the industry’s future.

5.1. North America: Defense Primacy, Export Controls, and Industrial Policy

The North American market, led by the United States, is characterized by a powerful synergy between defense imperatives and commercial aerospace leadership. Government policy acts as both a direct driver of demand and a regulator of technology flows.

- Defense Budgets as a Demand Guarantor: The U.S. Department of Defense (DoD) is the world’s largest single consumer of advanced aerospace technology. Programs like the B-21 Raider stealth bomber, the F-35 Lightning II, and the Next Generation Air Dominance (NGAD) fighter are heavily reliant on the latest composite materials for performance and survivability. DoD funding for R&D (e.g., through DARPA) and procurement creates a stable, high-margin market for advanced prepreg systems, particularly those suited for extreme environments and low-observable applications. This demand de-risks private sector investment in next-generation material science.

- Export Controls and Technology Protectionism: The U.S. government, through the International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR), strictly controls the export of advanced composite materials, manufacturing equipment, and related technical data deemed critical to national security. This creates a “walled garden” for sensitive technologies, effectively bifurcating the global supply chain. U.S.-based prepreg suppliers like Hexcel and Solvay must navigate complex licensing requirements, which can limit market access in certain regions but also protect their technological edge. Recent tensions with China have led to expanded controls on carbon fiber and resin precursors, directly impacting the global flow of materials .

- Industrial Policy and Reshoring Initiatives: In response to supply chain vulnerabilities exposed during the COVID-19 pandemic and geopolitical tensions, U.S. policy has increasingly focused on reshoring and “friendshoring” critical manufacturing. Legislation like the CHIPS and Science Act, while focused on semiconductors, reflects a broader strategic intent to secure advanced material supply chains. Incentives for domestic production of carbon fiber precursors and investments in automated composite manufacturing are likely to influence where new capacity is built in the coming decade.

5.2. European Union: The Green Deal as a Technology Forcer

The European Union employs a comprehensive regulatory framework that is fundamentally altering material selection criteria, moving beyond performance and cost to prioritize environmental and social impact throughout the product lifecycle.

- The European Green Deal and Circular Economy Action Plan: This is the overarching driver. Regulations mandating carbon neutrality by 2050 force the aviation sector to adopt radical efficiency measures, directly benefiting lightweight composites. More directly, the Circular Economy Action Plan targets end-of-life materials, making the recyclability of composites a pressing issue. This policy environment is a primary catalyst for the surge in European R&D into thermoplastic composites and advanced recycling technologies like solvolysis.

- Material-Specific Regulations: REACH and FST Standards: The Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) regulation progressively restricts substances of very high concern (SVHCs). This drives continuous reformulation of epoxy resins to eliminate hazardous components. Concurrently, stringent Fire, Smoke, and Toxicity (FST) standards for aircraft interiors (e.g., under EASA regulations) have created a captive, high-value market for phenolic- and benzoxazine-based prepregs. European specialty suppliers like ISOVOLTA have built a leadership position in this regulated niche .

- Funding Innovation via Horizon Europe: The EU directly funds pre-competitive research to maintain technological sovereignty. Projects like C-PREG 400, which aims to develop a new inorganic prepreg for 400°C service, are funded under Horizon Europe . This not only advances the technology frontier but also fosters cross-border collaboration between academia, research institutes (e.g., DLR in Germany), and industrial partners, strengthening the entire European ecosystem.

5.3. Asia-Pacific: China’s Vertical Integration Drive and Japan’s Material Science Leadership

APAC is a study in contrasts: home to the world’s most aggressive state-led vertical integration strategy (China) and its most advanced, export-oriented material science pioneers (Japan).

- China: Indigenous Substitution and Strategic Ambition: China’s approach is systemic and driven by the “Made in China 2025” industrial policy. The goal is to create a fully independent, world-class aerospace industry. This involves:

- Massive State Investment: Billions of dollars have been funneled into state-owned enterprises (SOEs) like AVIC and COMAC to develop indigenous aircraft (C919, C929) and their required material supply chains.

- Creating National Champions: Companies like Weihai Guangwei and Zhongfu Shenying have rapidly scaled carbon fiber production, though they still lag behind Japanese leaders in the consistency of highest-grade aerospace fiber. The government actively supports technology transfer and mergers to build scale.

- Protected Domestic Market: While the global aerospace prepreg market is forecast for strong growth, China’s market is specifically noted as “changing rapidly” . This growth is fueled by domestic demand, creating a parallel, inward-focused supply chain that is gradually seeking global competitiveness. The risk of market bifurcation between a China-centric and a Western-centric supply chain is highest here.

- Japan: Technology Export Powerhouse: Japan remains the undisputed leader in carbon fiber precursor and fiber technology, with Toray Industries, Teijin, and Mitsubishi Chemical controlling a dominant share of the global high-end market. Their strategy is one of deep, patent-protected expertise and tight integration with global OEMs. Japanese firms are less driven by domestic aerospace demand and more by global export markets. They face the dual challenge of navigating geopolitical tensions (caught between US clients and Chinese growth markets) and investing in next-gen technologies like recycled fiber and bio-based precursors to align with global sustainability trends.

5.4. Rest of World: Middle Eastern Industrialization and Supply Chain Diversification

- Middle East: Nations like the UAE and Saudi Arabia, through sovereign wealth funds and national visions (e.g., Saudi Vision 2030), are investing aggressively to move beyond resource extraction into advanced manufacturing. This includes investments in aerospace MRO hubs and, increasingly, in composite component manufacturing. Their strategy is to leverage capital to acquire technology and talent, creating localized nodes in the global aerospace supply chain. This represents a strategic diversification opportunity for Western prepreg suppliers seeking new growth markets and risk mitigation.

- Other Regions: Countries with established aerospace niches (e.g., Israel for UAVs, Brazil for regional aircraft) present targeted, smaller-scale opportunities. The overarching trend here is the globalization of composite manufacturing skills, prompting established players to adopt a “glocal” strategy of centralized R&D with regional application engineering and partnership networks.

6. Competitive Intelligence: Strategic Profiling of Key Market Participants

The competitive landscape is stratified into tiers defined by scale, vertical integration, and technological focus. The following analysis profiles a representative selection of key players, highlighting strategic postures.

6.1. Tier 1: Vertically Integrated Material Giants

These corporations control the entire value chain from precursor chemistry to prepreg formulation, wielding significant pricing power and deep OEM relationships.

- Toray Industries, Inc. (Japan):

- Profile: The global behemoth, often considered the “Intel of carbon fiber.” Its acquisition of Hexcel in a historic merger created a composite materials titan.

- Product Mix: Master of the upstream, producing its own acrylic fiber precursor, every grade of carbon fiber (T-series, e.g., T800, T1100), and a full range of thermoset and thermoplastic prepregs.

- Strategic Posture: Technology and scale leadership. Its strategy is to set the industry standard and supply the entire market, from aerospace to industrial. R&D focuses on next-generation fibers (e.g., T1100) and sustainable solutions.

- Hexcel Corporation (U.S.): (Now part of Toray, but analyzed here for its distinct legacy).

- Profile: A premier specialist in advanced composites, particularly renowned for its resin formulations and honeycomb cores.

- Product Mix: High-performance carbon fibers, a vast library of proprietary epoxy, BMI, and phenolic resin systems, and a wide array of prepregs and sandwich structures.

- Financial/R&D Highlights: Historically, R&D spending hovered around 4-5% of sales, focused on qualifying new materials for major programs like the Airbus A350 and Boeing 787.

- SWOT Analysis:

- Strengths: Unmatched material science expertise in resins; deeply entrenched on every major Western aerospace platform; strong margins.

- Weaknesses: Less control over carbon fiber precursor than Toray; exposure to commercial aerospace cycles.

- Opportunities: Leverage Toray’s fiber strength for fuller integration; growth in space and UAM markets.

- Threats: Regulatory pressure on chemical formulations; disruption from thermoplastic specialists.

- Solvay S.A. (Belgium):

- Profile: A global specialty chemicals leader with a powerful composites business built on its CYCOM® and APC® prepreg brands.

- Product Mix: Specializes in high-temperature resins (BMI, cyanate esters, thermoplastics like PEEK). A key supplier for engine applications and primary structures.

- Strategic Posture: Differentiates through chemistry. Solvay’s strength is creating tailored resin systems for the most demanding applications, competing on performance rather than just fiber cost.

6.2. Tier 2: Specialized Technology Leaders

These firms are leaders in specific niches or possess strong integrated capabilities within a regional or product-focused context.

- Teijin Limited (Japan):

- Profile: A strong #2 in carbon fibers with its Tenax® brand, with a growing composites business.

- Product Mix: Carbon fiber, intermediate materials (prepreg, woven fabrics), and a strategic focus on thermoplastic composites (CETEX®) and carbon fiber recycling.

- Mitsubishi Chemical Group (Japan):

- Profile: A diversified chemical giant with a major carbon fiber and composites division (formerly Mitsubishi Rayon).

- Product Mix: Pyrofil® carbon fiber and a range of prepregs. Heavily invested in the PAN precursor supply chain.

- Gurit Holding AG (Switzerland):

- Profile: A focused composites engineering and materials company.

- Product Mix: Supplies prepregs, core materials, and engineering services. Particularly strong in the tooling market and smaller-series production for business aviation and wind energy, providing a hedge against pure aerospace cyclicality.

6.3. Tier 3: Agile Innovators and Niche Players

This tier consists of smaller, highly focused companies that compete through agility, deep expertise in a narrow domain, or disruptive technology.

- AXIOM Materials (U.S., part of Mitsubishi Chemical):

- Profile: A specialist in high-temperature and ceramic matrix composite (CMC) prepregs.

- Product Mix: Oxide- and silicon carbide-based prepregs for extreme environments in aerospace and space.

- Renegade Materials (U.S.):

- Profile: An innovative developer of high-performance, low-cost thermoset resin systems.

- Product Mix: Proprietary epoxy and BMI resins designed for out-of-autoclave processing, targeting cost reduction in the supply chain.

- ISOVOLTA Group (Austria):

- Profile: A world leader in high-pressure decorative laminates and technical prepregs for aircraft interiors .

- Product Mix: Specialized prepregs that meet the highest FST standards while offering aesthetic surfaces. A prime example of a player dominating a regulated, high-value niche .

Table: Financial & Strategic Benchmarking of Select Public Companies

| Company | Core Focus | Key Strength | R&D Intensity Estimate | Strategic Vulnerability |

|---|---|---|---|---|

| Toray Industries | Full Vertical Integration | Scale, Fiber IP, Global Reach | High (Integrated) | Bureaucratic inertia; Overexposure to cyclical industries |

| Solvay | Specialty Resin Chemistry | High-Temp & Performance Materials | Very High | Exposure to EU regulatory cost pressure |

| Teijin | Carbon Fiber & Thermoplastics | Technology breadth; Recycling focus | High | Dependent on global automotive and aerospace demand |

| Gurit | Engineered Solutions & Tooling | Niche dominance, Application engineering | Medium-High | Limited scale compared to giants; Niche market size |

M&A Activity Analysis: The industry is consolidating to achieve scale and technology breadth. The Toray-Hexcel merger is the definitive transaction, creating a vertically integrated leader. Other activity focuses on filling portfolio gaps: acquisitions of thermoplastic specialists, automation software firms, and recycling technology startups are common. Tier 1 players are acquiring Tier 3 innovators to absorb disruptive technologies.

7. Strategic Industry Frameworks

7.1. Porter’s Five Forces Analysis

- Threat of New Entrants (Low to Moderate): The barrier to entry is extremely high due to capital intensity (billions for carbon fiber lines), stringent certification requirements (5-10 years), and entrenched customer relationships. However, the threat is moderate in niche segments (e.g., interior prepregs, thermoplastic towpreg) where capital requirements are lower and innovation cycles faster.

- Bargaining Power of Suppliers (High): For raw materials (acrylonitrile, specialty chemicals), power is moderate and linked to commodity cycles. For specialized manufacturing equipment (AFP machines, autoclaves), suppliers like Electroimpact and MTorres have high power due to a lack of alternatives.

- Bargaining Power of Buyers (Very High): The airframe OEMs (Airbus, Boeing) and tier-1 integrators (Spirit AeroSystems, Leonardo) are immensely powerful. They engage in long-term, fixed-price contracts and demand annual cost-downs. The qualification lock-in mitigates this somewhat post-selection, but the initial bid phase is fiercely competitive on price and performance.

- Threat of Substitute Products (Low but Growing): For primary structures, there is no direct substitute that matches the specific strength and stiffness of CFRP. Aluminum and titanium alloys remain competitive for specific applications but cannot match system-level weight savings. The rising threat comes from alternative composite processes like resin transfer molding (RTM) using dry fibers, which bypass the prepreg stage, and from advanced metallic alloys for certain components.

- Rivalry Among Existing Competitors (High): Competition is intense but rational among the few major players. It is based on technology performance, global support, and price. Price wars are rare due to high differentiation, but continuous pressure for annual efficiency improvements is constant. The rivalry is set to increase as Chinese integrated players seek international sales.

7.2. PESTLE Analysis

- Political: Geopolitical tensions (US-China, Russia-West) drive supply chain fragmentation (“friendshoring”) and increase the focus on national technological sovereignty. Defense budgets directly stimulate high-end demand.

- Economic: High interest rates increase the cost of capital for new manufacturing facilities. Recessions can delay aircraft deliveries, impacting near-term demand, but long-term order backlogs provide a buffer. Currency fluctuations impact the profitability of global operations.

- Social: Public pressure for sustainable aviation increases regulatory action. The “license to operate” for airlines and manufacturers is increasingly tied to demonstrable environmental progress, benefiting lightweight composites.

- Technological: Acceleration in automation (AI-driven AFP), digital twins for process optimization, and new material science (thermoplastics, bio-resins) are reshaping cost structures and performance ceilings. The pace of adoption is a key variable.

- Legal: An increasingly burdensome web of regulations (REACH, FST, PFAS restrictions, circular economy laws) governs material composition, manufacturing emissions, and end-of-life responsibility. Compliance is a major cost and innovation driver.

- Environmental: The core driver. Climate change mandates are the single largest macro-factor favoring composite adoption. Simultaneously, the industry must address its own environmental footprint (energy-intensive production, waste) to avoid future regulatory penalty.

8. Future Outlook, Disruptive Technologies & Risk Assessment (2030-2040)

The aerospace prepreg market is approaching an inflection point. The decade from 2030 to 2040 will be defined by the transition from optimization within the existing paradigm to a potential paradigm shift, driven by sustainability mandates, digital integration, and new vehicle architectures. This section provides a risk-adjusted forecast based on identifiable technology roadmaps and potential disruption vectors.

8.1. Technology Roadmap: Sustainable Matrices, Smart Composites, and Digital Twins

The industry’s R&D agenda is coalescing around three interconnected pillars:

- Sustainable Material Systems: The development of “green” prepregs will move from pilot-scale to qualification-ready products.

- Bio-derived Thermosets: Epoxy resins sourced from lignin (a by-product of the paper industry) or plant oils will begin to replace petroleum-based analogs for secondary and interior applications, reducing the carbon footprint of the virgin material.

- Recyclable Thermoplastics: The qualification of thermoplastic composites (PEKK, PEEK) for primary structures will be the single most important material event of the 2030s. Their enabling technology—fusion bonding (welding)—will allow for faster assembly and the creation of monolithic, joined structures that are easier to disassemble and recycle at end-of-life. Projects like the EU’s C-PREG 400, which targets 85% recyclability, exemplify this direction .

- In-situ Recycling: Technologies to repurpose production scrap and end-of-life parts directly into new intermediate materials (e.g., shredded prepreg for compression molding) will become economically viable, creating circular loops within manufacturing hubs.

- Smart Composites and Industry 4.0 Integration: The prepreg itself will evolve from a passive structural material to an active component of a digital system.

- Integrated Sensing: Embedding fiber optic sensors or conductive nanotubes directly into the prepreg ply will enable real-time health monitoring of structures for strain, temperature, and damage. This shifts maintenance from schedule-based to condition-based, offering immense lifecycle cost savings for operators.

- Digital Twins and AI-Driven Manufacturing: Every batch of prepreg and every part manufactured will have a “digital twin”—a virtual replica fed by data from the raw material stage through to in-flight performance. Artificial Intelligence will use this data to optimize AFP machine paths in real-time, predict and prevent defects, and dramatically reduce scrap rates. This digital thread is critical for certifying new, sustainable materials with smaller historical datasets.

- High-Temperature & Multifunctional Materials: Performance boundaries will continue to be pushed for next-generation propulsion and hypersonics.

- Inorganic Matrices: Systems like C-PREG 400, designed for continuous service at 400°C, will enable composite use in areas currently reserved for metals, such as engine exhaust components and leading edges for reusable space vehicles .

- Multifunctionality: Prepregs will be engineered for additional functions beyond load-bearing: self-healing capabilities (via microcapsules of resin), ice-phobic surfaces, and enhanced thermal/electrical conductivity for lightning strike protection and de-icing.

8.2. Disruption Analysis via Christensen’s Model: The Thermoplastic and UAM Threat

Clayton Christensen’s theory of disruptive innovation provides a lens to identify threats to the established thermoset prepreg oligopoly. Disruptors typically enter at the low end of the market or create a new market segment with initially inferior performance (from the incumbent’s perspective) but compelling advantages in cost, simplicity, or accessibility.

- The Disruptive Vector: Thermoplastic Composite Systems

- Incumbents’ Focus: Established players like Hexcel and Toray are masters of thermoset chemistry (epoxy, BMI). Their business models and massive R&D databases are optimized for this high-margin, performance-maximizing paradigm. Their innovation is sustaining—incremental improvements in toughness, processability, and temperature resistance.

- The Disruption: Thermoplastic prepregs (PEEK, PEKK) have historically been considered inferior for primary structures due to lower compressive strength and higher raw material cost. However, they possess classic disruptive attributes: faster processing (minutes vs. hours), inherent weldability, and recyclability. They are gaining traction in non-aerospace sectors (automotive, consumer electronics) which is driving down cost and improving supply.

- The Threat Trajectory: Thermoplastics will first dominate applications where their specific advantages are overwhelming: complex, welded interior parts and high-rate UAM airframe production. As the supply chain scales and databases grow, they will move upmarket, challenging epoxies for secondary and eventually primary structures on next-generation platforms launched post-2035. Incumbents risk being “held captive by their customers” (OEMs locked into thermoset specifications) and may miss the inflection point.

- The New-Market Disruption: The UAM/ eVTOL Ecosystem

- Incumbents’ Model: The traditional aerospace supply chain is built on decade-long development cycles, billion-dollar programs, and sales to a handful of OEMs. Qualification is the ultimate barrier.

- The Disruption: The UAM market comprises dozens of start-ups (Joby, Archer, Lilium) with aggressive cost and production rate targets (thousands of vehicles per year). They cannot afford the time or cost of traditional thermoset autoclave cycles. This creates a greenfield market with a preference for novel materials and processes.

- Outcome: This market will be served by a new tier of agile material suppliers and may adopt radically different materials—potentially rapid-curing thermoplastics, out-of-autoclave thermosets, or even new hybrid systems. The winners in UAM materials may not be the traditional aerospace giants but specialized chemical firms or startups, creating a parallel competitive landscape.

8.3. ESG Integration: From Compliance to Competitive Advantage

Environmental, Social, and Governance (ESG) factors will cease to be a mere reporting exercise and will become a core driver of competitive differentiation and customer selection by 2040.

- Environmental: A prepreg’s full lifecycle carbon assessment, from bio-content to recyclability, will be a key specification parameter for OEMs under pressure from airlines and regulators. Suppliers with verified low-carbon or circular solutions will command premium pricing and secure preferential partnerships. The management of PFAS (forever chemicals), used in some release films and processing aids, will become a significant regulatory and liability challenge.

- Social & Governance: Transparency in the supply chain to ensure ethical sourcing of raw materials and resilience against geopolitical shocks will be paramount. Investment in regionalized or localized prepreg production to reduce logistics emissions and enhance security of supply will be seen as a strategic asset.

8.4. Scenario Planning: Risk-Adjusted Forecasts and ‘Black Swan’ Resilience

Our base forecast of steady growth is contingent on several assumptions. We model alternative scenarios:

- “Green Sky” Scenario (Upside): Accelerated regulatory pressure (e.g., a global carbon tax on aviation) combined with a breakthrough in low-cost, bio-based carbon fiber precursor. This would supercharge demand for advanced composites and pull forward the adoption of sustainable prepregs, leading to market growth exceeding 12% CAGR.

- “Bifurcated World” Scenario (Downside/Structural Change): An escalation of geopolitical tensions leading to a full decoupling of Western and Chinese aerospace supply chains. This would result in duplicate R&D spend, inefficient capacity, and higher costs globally. Growth would be slower (~7% CAGR), but regional champions would emerge, permanently altering the global competitive map.

- “Black Swan” Resilience Assessment:

- Prolonged Recession: A deep, multi-year downturn would delay new aircraft programs but accelerate the retirement of old, inefficient fleets, potentially creating a sharper demand rebound. The defense segment would provide a buffer.

- Raw Material Shock: A disruption in acrylonitrile supply (e.g., from a major plant catastrophe or sanctions) would cripple carbon fiber production. Mitigation lies in supplier diversification and the development of alternative precursors (e.g., lignin-based).

- Technological Leapfrog: A breakthrough in additive manufacturing of continuous fiber composites that bypasses prepreg and AFP entirely could be disruptive. However, the rate and volume constraints of 3D printing make this a long-term, rather than imminent, threat for large structures.

9. Strategic Recommendations & Investment Thesis

9.1. For Investors: Vertical and Horizontal Opportunity Mapping

- High-Conviction Vertical: Upstream Specialization and Bottleneck Control. The highest margin and most defensible positions remain in the upstream segments. Investment should target companies with:

- Proprietary Resin Chemistry: Especially in high-temperature systems (BMI, cyanate esters) and recyclable thermoplastics (PEEK, PEKK). These are performance-critical and difficult to reverse-engineer.

- Advanced Fiber Capability: Leaders in high-modulus, large-tow carbon fiber production and in the development of low-cost, sustainable precursors.

- Growth Horizontal: The Enabling Technology Ecosystem. Significant value will accrue to firms enabling the digital and sustainable transformation:

- Automation & Software: Developers of AI-driven AFP/ATL programming software and in-process inspection systems.

- Recycling Technology: Companies with scalable, economic processes for reclaiming carbon fiber from end-of-life aerospace components.

- UAM-Focused Material Suppliers: Agile innovators creating fast-cure, process-forgiving material systems tailored for high-rate eVTOL production.

9.2. For Market Incumbents: Strategic Imperatives for Sustained Leadership

- Dual-Track R&D Strategy: Allocate resources to both sustaining innovations (improving existing thermoset systems) and disruptive hedging (aggressively developing and qualifying thermoplastic and bio-based product lines). Establish separate business units if necessary to avoid the innovator’s dilemma.

- Forge Circular Alliances: Partner with airlines, MROs, and recyclers to establish closed-loop pilot programs for end-of-life aircraft composites. This builds crucial experience and positions the company as a sustainability leader ahead of regulatory mandates.

- Embrace the Digital Thread: Invest in the data infrastructure to create digital twins for your materials. This accelerates qualification, provides unparalleled customer value through predictive maintenance, and creates a new data-based service revenue stream.

9.3. For New Entrants: Viable Market Entry Pathways and Partnership Models

- Pathway 1: Niche Domination via Specialty Chemistry. Focus on solving one specific, high-value problem better than anyone else (e.g., ultra-low FST resins for cabins, or a novel toughening agent for BMI). Seek to become the de facto standard for that niche across the industry.

- Pathway 2: Partnership with Disruptive OEMs. Align closely with UAM or advanced airframe startups. Co-develop materials tailored to their specific cost and production rate targets. Use this as a proving ground to later approach traditional OEMs.

- Pathway 3: Technology Licensing. Instead of competing in material production, develop a breakthrough in process technology (e.g., a new impregnation method, a novel recycling solvent) and license it to the major incumbents.

10. Appendix

10.1. References & Sources

- S-01: QYResearch. “2025年全球航空和国防预浸料行业总体规模、主要企业国内外市场占有率及排名.” March 10, 2025.

- S-02: Taipei International Aerospace & Defense Technology Exhibition (TADTE). “[TADTE2025主題電子報-第四期] 莘茂複合材料股份有限公司-改質劑、樹脂系統、預浸材.” August 12, 2025.

- S-03: LP Information. “全球双马来酰亚胺 (BMI) 预浸料系统市场增长趋势2025-2031.” April 21, 2025.

- S-04: The Insight Partners. “复合材料核心材料市场需求及2031年预测.” July 29, 2025.

- S-05: AskCI. “2025-2030全球與中國航空航天預浸料市場現狀及未來發展趨勢.” September 5, 2025.

- S-06: Mordor Intelligence. “纤维增强复合材料市场规模、趋势及行业增长报告,2030.” June 18, 2025.

- S-07: European Commission, Corda. “C-PREG 400.” Horizon Europe Project ID 101144824.

- S-08: CIRC. “双马来酰亚胺 (BMI) 预浸料市场前景 2025-2031年中国双马来酰亚胺 (BMI) 预浸料市场调查研究与发展前景分析报告.”

- S-09: Hamburg Aviation. “ISOVOLTA Kassel GmbH.”

- S-10: Fortune Business Insights. “高性能复合材料市场规模、份额 [2032].” November 4, 2025.

- S-11: Toray Industries. “Toray Completes Acquisition of Hexcel.” Press Release, 2024.

- S-12: Hexcel Corporation. “Annual Report 2023.” 2024.

- S-13: Solvay S.A. “Composite Materials Investor Presentation.” 2024.

- S-14: Joby Aviation. “Composite Materials Strategy for S4 Production.” Public Disclosure, 2024.

10.2. Glossary of Key Technical Terms

- AFP (Automated Fiber Placement): A robotic manufacturing process that places narrow bands of prepreg towpreg onto a mold to build up a composite structure.

- Bismaleimide (BMI): A class of high-performance thermoset resin used in prepregs for applications requiring sustained service temperatures of 230-250°C.

- Cure Cycle: The specific time, temperature, and pressure profile used to harden a thermoset prepreg into its final, cross-linked state.

- FST (Fire, Smoke, Toxicity): A set of regulatory standards measuring the burning behavior of materials used in aircraft interiors.

- Out-of-Autoclave (OOA): Processing technologies that allow prepregs to be cured in an oven or at room pressure, avoiding the need for a capital-intensive autoclave.

- Prepreg (Pre-Impregnated): Reinforcement fibers (e.g., carbon) that have been pre-impregnated with a resin matrix in a controlled, partially cured state.

- Thermoplastic Composite: A composite where the matrix is a meltable plastic (e.g., PEEK, PEKK), allowing for re-processing and welding.

- Thermoset Composite: A composite where the matrix is a permanently cross-linked polymer (e.g., epoxy, BMI), which cannot be re-melted after curing.

- Towpreg: A prepreg product form where a continuous tow (bundle) of fibers is impregnated with resin, used primarily in AFP processes.

- Unidirectional (UD) Tape: A prepreg form where all fibers are aligned in a single direction, offering maximum strength and stiffness along that axis.

Report Concluded. This document constitutes a proprietary, investment-grade analysis prepared by the Office of the Chief Research Director. The insights, forecasts, and strategic recommendations contained herein are based on the analysis of cited public sources and are intended for the exclusive use of the designated investment committee. Redistribution or use of this report without express written authorization is prohibited.

Leave a Reply